Affinity is launching Ascend, an agent platform for private capital, and stepping into a new identity as the AI-first private capital CRM. A note from our CEO.

Learn more →

Learn more →

Becoming fluent in AI was never the job

You came into private capital to close deals, not to learn a dozen AI tools. Affinity Ascend takes the busywork off the deal, so the work can be all that's left.

Learn more →

Learn more →

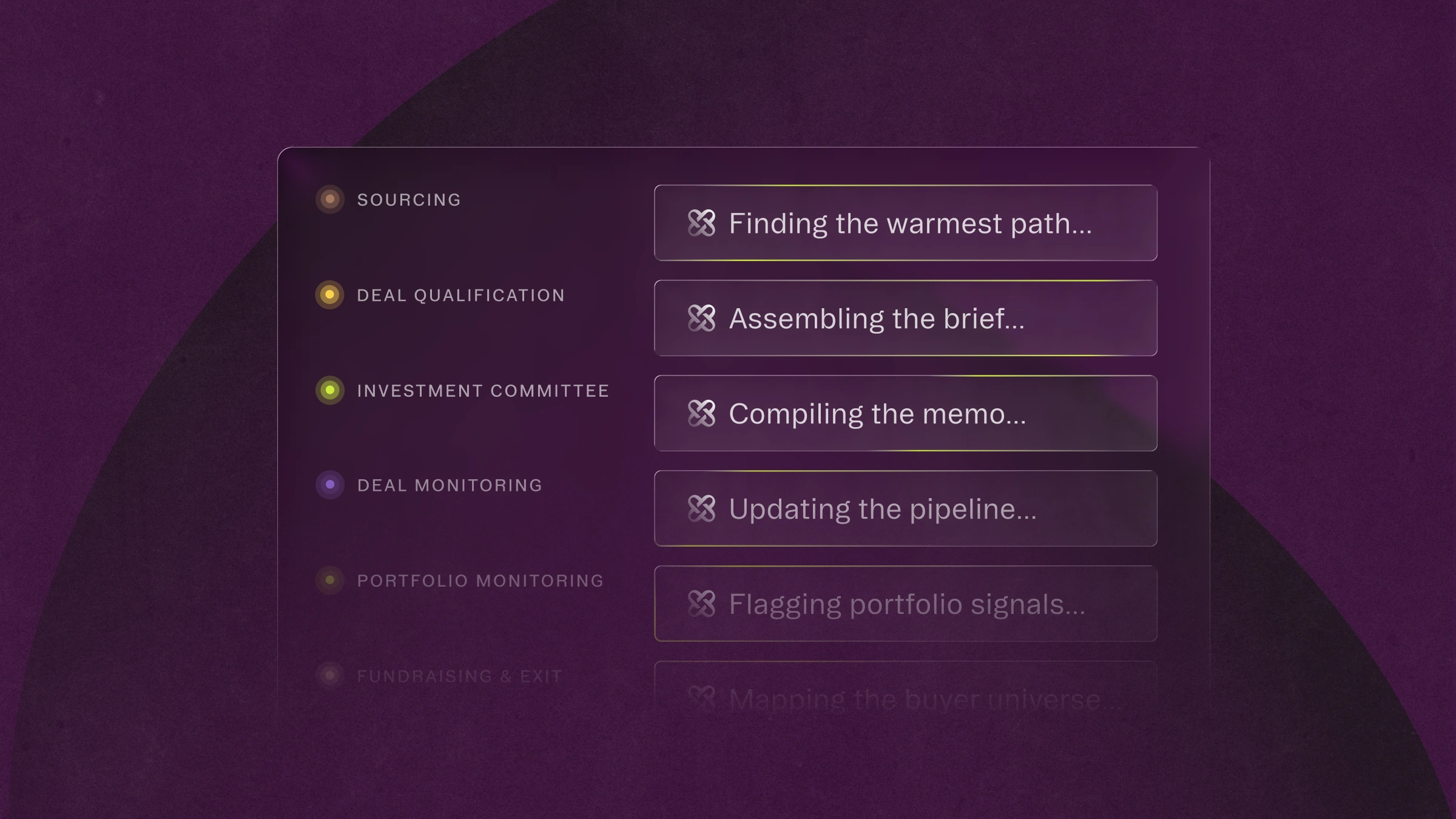

Introducing Affinity Ascend

Affinity Ascend is the agent platform for private capital. Three agents are live on launch—Meeting Prep, Warm Intros, and Data Update. Here's what ships and how to use it.

Learn more →

Learn more →

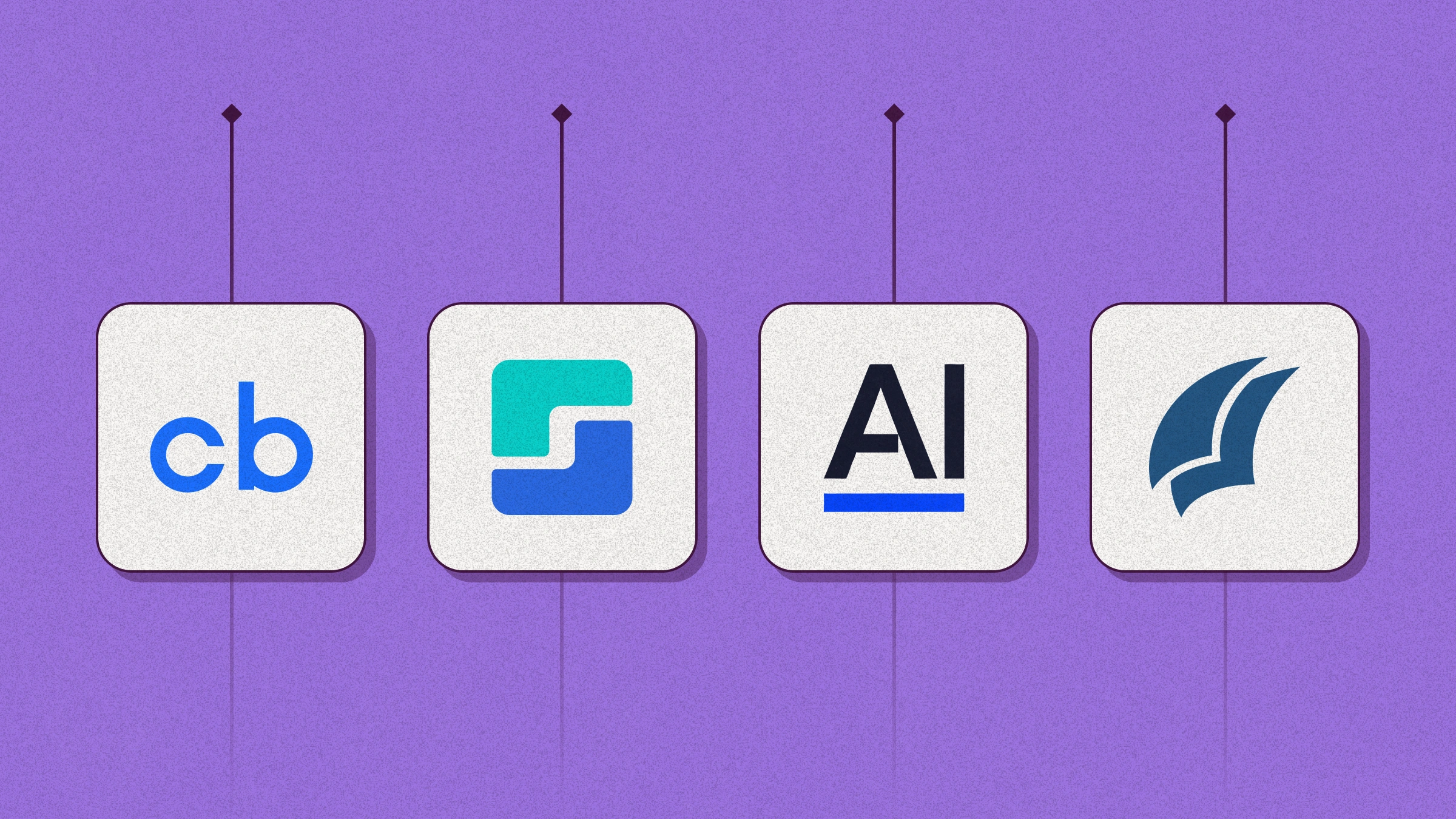

Your AI doesn't know your firm. Connect it to the tools that do.

Four AI workflows across the deal lifecycle—Grata, Crunchbase, AlphaSense, and Lumonic—each connected to Affinity so your model reaches your pipeline, relationships, and data.

Learn more →

Learn more →

Brand or expertise: the 2x2 that decides which PE firms pull ahead

Most middle-market private equity firms can't say what they do better than anyone else. A former Citi CFO's 2x2 for finding your firm's real edge.

.webp)

.webp)