2025 private capital outlook in numbers

Each year, we ask hundreds of private capital professionals about their industry outlook. Our questions cover everything from deal volume expectations and fundraising opportunities to the ways that firms are using AI.

While we compiled our findings for 2025 in our annual private capital predictions report, we wanted to share the data that didn’t get as much attention.

Read on for the raw metrics from our 2025 Private Capital Predictions Survey across dealmaking, data, AI, and fundraising. We’ll also show how these metrics stack up by region, firm size, or time period where there are the most notable differences.

If you’re looking for an analysis of these metrics, the key factors driving private capital in 2025, and how to prepare for them, be sure to check out our predictions report.

Our survey respondents

We surveyed 297 private capital professionals across venture capital, corporate venture capital, private equity, growth equity, accelerator, and incubator segments.

Our survey was global, with the majority (60%) of respondents working in North America, followed by 31% in EMEA, 7% in Asia and Oceania, and 2% in South America. In terms of firm size, 74% of respondents were from firms with 30 or fewer employees while the remaining 26% were from firms with more than 30 employees (which we’ll call “larger firms”).

Here are the raw metrics from the survey:

Dealmaking

What are your deal volume expectations for 2025 (compared to 2024)?

Global vs. EU-only

_.webp)

Key takeaway: Both global and EU-only respondents are optimistic about dealmaking in 2025, with EU respondents showing greater optimism.

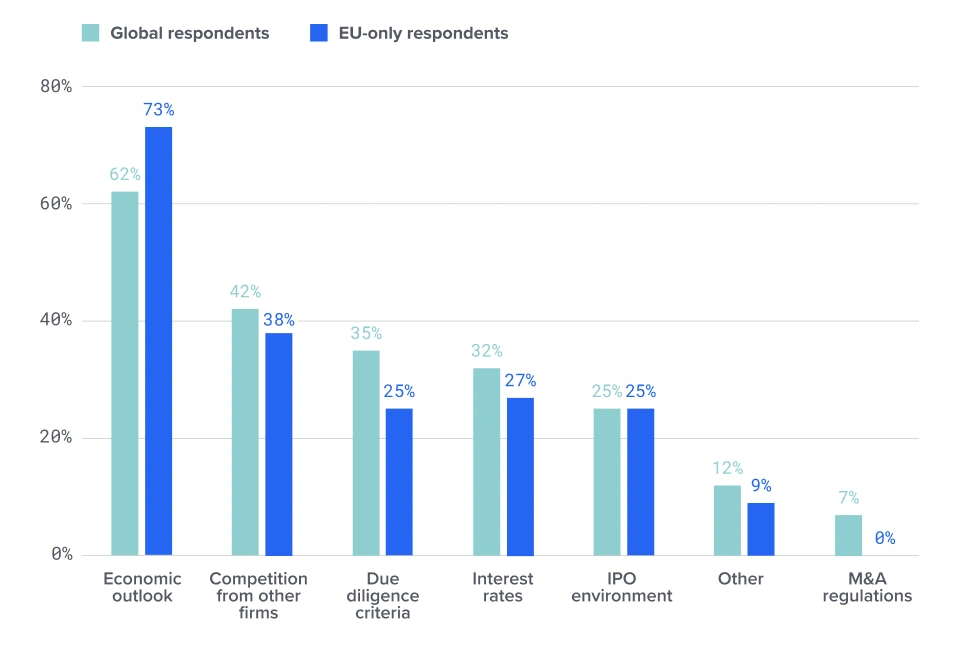

Which of the following factors do you expect to significantly impact your deal volume in 2025?

Global vs. EU-only

Key takeaway: The majority of respondents expect the economic outlook to be the primary factor impacting deal volume in 2025, followed by competition from other firms. With central bank rate cuts underway and the U.S. election behind us, expectations for improving market conditions appear to be fueling deal optimism globally.

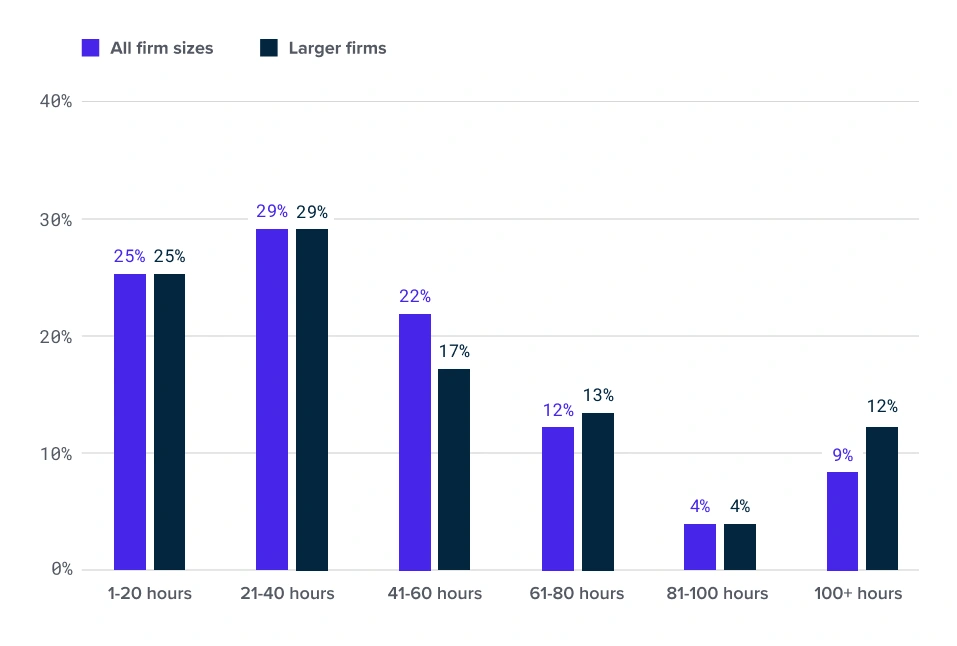

How many hours on average do you spend researching a deal?

All firm sizes vs. Larger firms

Key takeaway: The majority (54%) of firms spend 40 or fewer hours researching a deal. Larger firms spend more time in extended research, with higher representation in both the 61-80 hour and 100+ hour ranges. This suggests that larger firms may have greater resources or tackle larger or more complex deals that require deeper analysis.

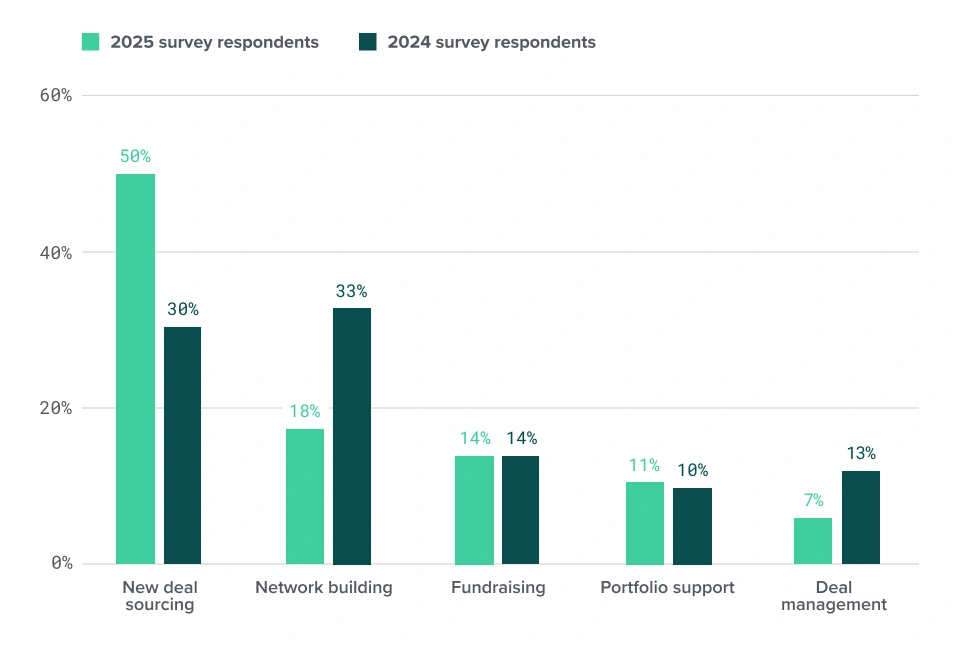

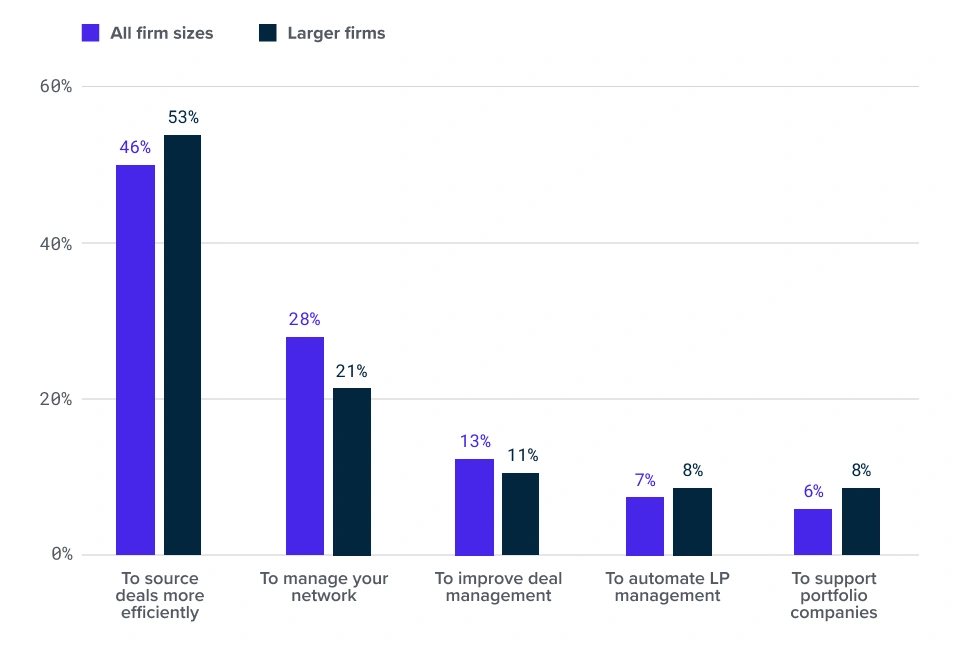

Which activity do you plan to dedicate the most time to in 2025?

2025 vs. 2024

Key takeaway: Investor priorities are changing, with a significant shift in focus to new deal sourcing compared to 2024. Read our predictions report to learn why (and how) investors are prioritizing deal sourcing in 2025.

Data and AI

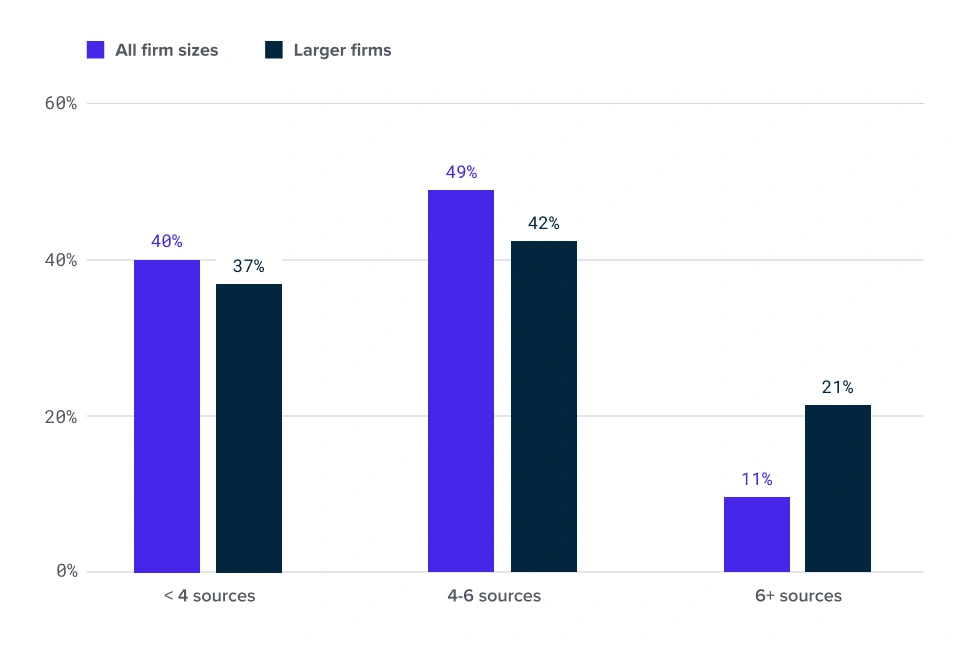

When deal sourcing, how many data sources do you rely on to evaluate an opportunity?

All firm sizes vs. Larger firms

Key takeaway: Larger firms rely on more data sources to evaluate deals, which aligns with their tendency to spend more time on extended research compared to smaller firms.

Where is the biggest opportunity for data in your investment operations?

All firm sizes vs. Larger firms

Key takeaway: With an increased focus on new deal sourcing, it’s no surprise that both all firms and larger firms are prioritizing efficiency in their sourcing processes.

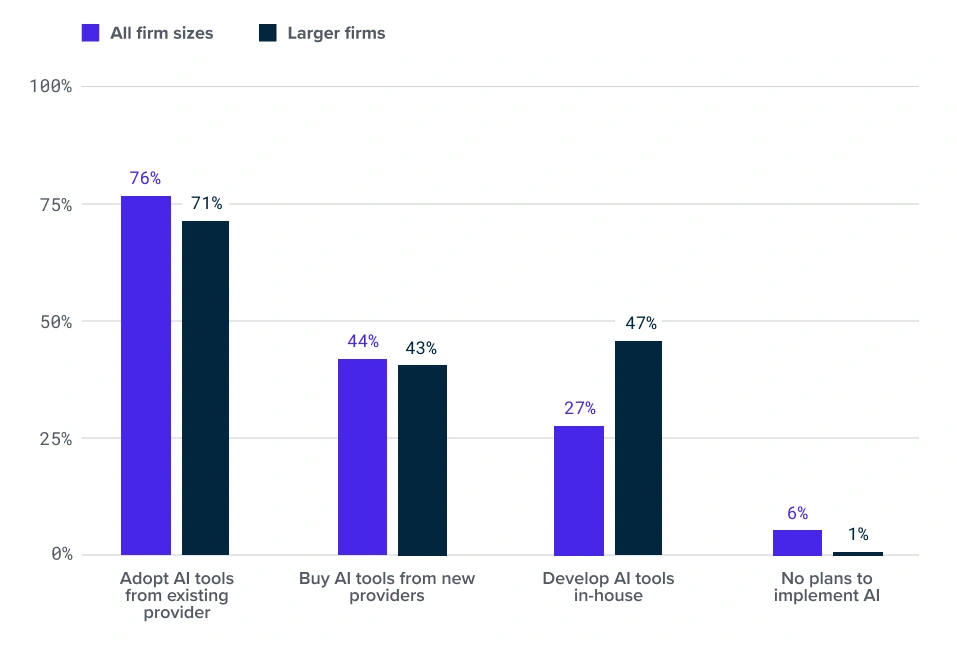

How is your firm planning to implement AI?

All firm sizes vs. Larger firms

Key takeaway: Most firms plan to use AI tools from their existing providers, however, a greater proportion of larger firms are also developing new AI tools in-house.

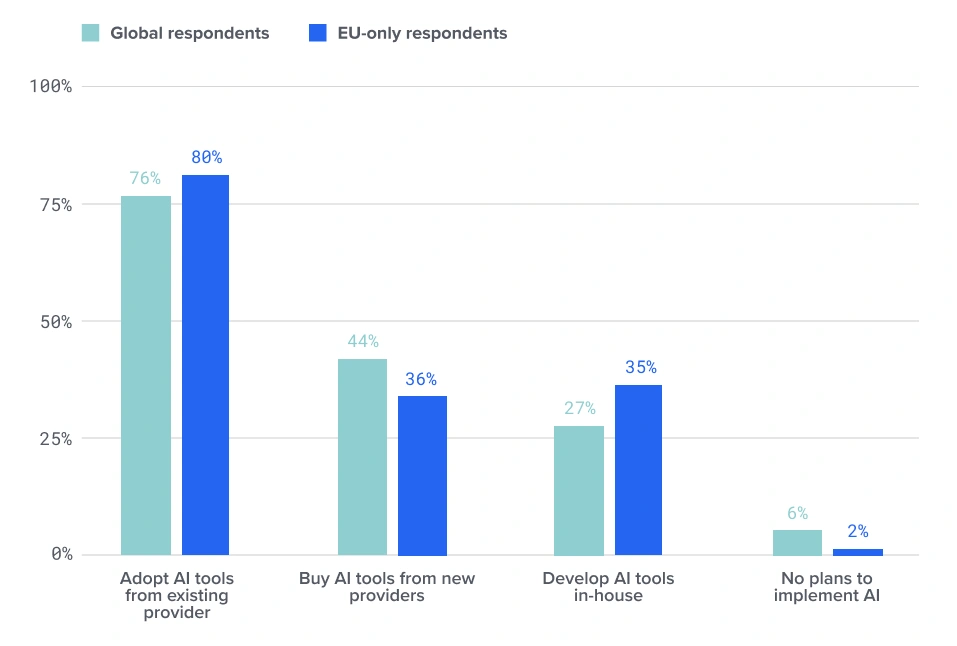

Global vs. EU-only

Key takeaway: Nearly all (98%) European respondents plan to implement AI, compared to 94% globally, suggesting they’re slightly more advanced on the AI front.How does your firm use AI?

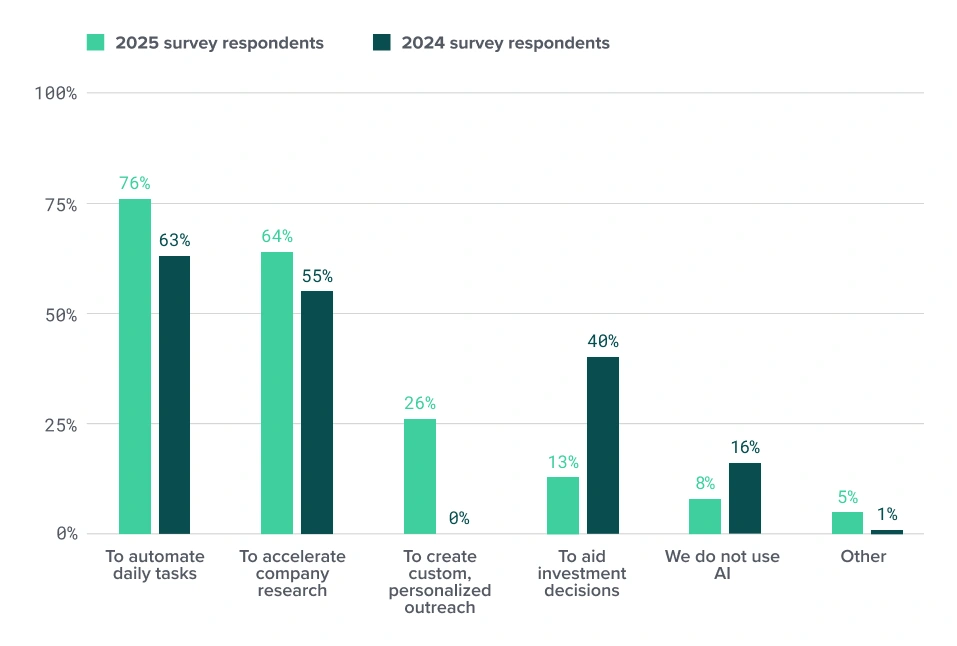

2025 vs. 2024

Key takeaway: Compared to 2024, there was a notable shift in how investors use AI—with more respondents using AI for productivity-related tasks (like automation and accelerating company research) and significantly fewer using it to help with investment decisions.

Fundraising

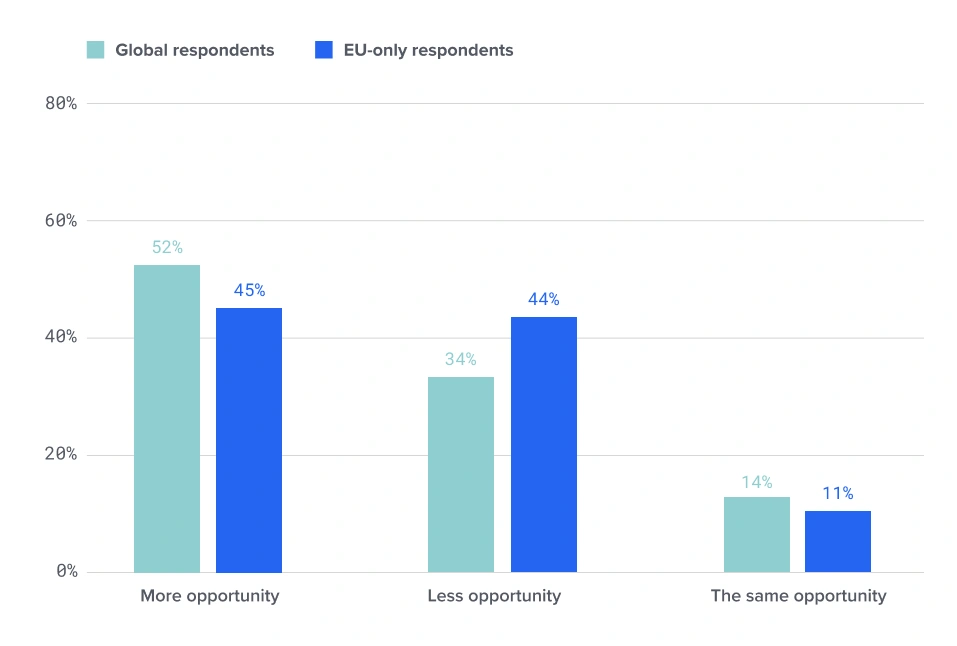

Do you see the opportunity to raise a fund in 2025 as greater, less, or the same in 2024?

Global vs. EU-only

Key takeaway: Across the board, the fundraising outlook is relatively subdued—with more caution from EU-only respondents.

Whether or not you plan to raise a fund in 2025, what’s the most challenging aspect of fundraising today?

Global vs. EU-only

Key takeaway: There are a number of challenges to fundraising in this environment, but proving the value of existing funds is top of mind for respondents globally—even more so in the EU. The pressure is on to close high-quality deals and deliver returns to LPs.

*The most common themes in 'Other' related to liquidity challenges and LP reluctance to invest with new funds or new managers.

Understand what’s driving private capital in 2025

Private capital is gearing up for a pivotal year. For an in-depth analysis of these metrics and the key themes shaping the industry in the year ahead, check out our 2025 private capital predictions report.

You’ll learn:

- Why investors are turning up the notch on deal sourcing

- How firms are using AI to tackle data complexities

- What investors are doing to stand out amidst greater competition

Related Articles

Put your firm’s network to work